Most if not all QSR’s would have experienced unpresidented growth in the Delivery and Drive Thru channels during Covid-19- Casual Dining businesses less so but those that acted swiftly, were able to pivot and most likely had already started offering delivery would have faired much better particularly in Victoria where lockdowns were most severe. The big question is how much of this growth is sustainable once Covid normal returns, restrictions are eased and consumers get out and about.

With restaurant dine in “off the table” for the best part of 8 months (in Victoria) and less so in other states which did not experience a second wave of Covid, QSR’s could focus on fast tracking enhancements in Drive Thru customer experience. This trend had already been a major focus for some of the larger players ie McDonald’s and KFC, and to a lesser extent brands like GYG, Oporto and Taco Bell. Contactless payment, ease of ordering, facility quality are all critical factors in Drive thru sales performance. Remember the focus should be on speed and efficiency. and if customers see a long queue of cars they will often look for a substitute brand located within close proximity of the preferred site.

What’s interesting is that many QSR’s have seen a shift and broadening in their customer base especially in Victoria where one of the few industries that traded all through Covid lockdowns were QSR Drive Thru’s & Delivery providers. So increased sales and a broadening of the customer base are the key takeaways. In difficult or uncertain times consumers often look to comfort food.

The question for the industry then becomes how much of the incremental sales will stick post Covid and how do I factor this into sales forecasting? Firstly, it’s highly likely post Covid Delivery sales will continue to increase with many brands experiencing double digit growth. The interesting point here is that it isn’t necessarily uniformed growth, we have seen some pretty incredible fluctuations across the board. In addition, delivery sales have taken off in Australia moreso that some neighbouring countries so this trend upwards will continue. Also, traditional dining times have been shifting for years, so now the challenge is how do we reduce the footprint of the restaurant knowing that Drive Thru and Delivery channels will continue to grow and as a result there is less demand for dine in now spread further across the day/night. We have even seen KFC rollout Drive Thru/Delivery only restaurants in NSW and SA.

Getting back to the question about accounting for the shift in sales – this becomes an issue when whatever method you used to forecast the sales potential of a restaurant (pre Covid)- now is severely disrupted. How does this shift impact the nearest franchisee when one restaurant is doing 20% more in delivery sales then projected?

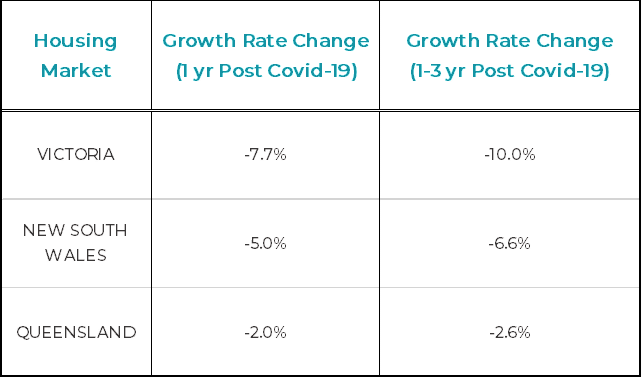

One of the determinant factors for growth more generally will be the impact on Greenfield housing development. The number of dwelling commencements occurring in greenfield development estates is influenced by two key drivers, broad area population growth (be it domestic or international) and economic prosperity.

Geotech foresees a significant slowing in new housing commencements over time, resulting in a slowing in population growth into new housing estate areas. There will however be a significant time lag for this slowing to properly manifest itself, and the level of impact will differ between regions and state markets.

Those markets with population growth more underpinned by overseas migration are likely to see a greater slowing in time. Additionally, those states whose economies have been most impacted post Covid-19 are also likely to see a greater slowing in new housing stock demand due to economic headwinds.

Greater Sydney and Melbourne have a greater proportion of population growth driven by overseas immigration. In 2019, 68% of Victoria’s and 62% of NSW’s annual population growth came from overseas migration. In comparison, only 48% of Queensland’s population growth came from overseas migration.

Victoria is also (as at August 2020) more likely to experience a greater economic impact post Covid-19. This is due to a combination of higher cases in Victoria resulting in harsher lock downs and a greater abundance of industries likely to be adversely impacted (or close) in the post Covid-19 world (such as education and research / finance / building).

There is a clear time lag between changes to new housing demand drivers, the commencement and completion of new housing stock and then resultant population growth in new growth areas as people occupy. This is particularly the case regards overseas migration, as typically new arrivals into Australia will not immediately build a new home in a new growth area. The time lag from this form of population growth seeking to build new housing can be considerable.

With this in mind, Geotech sees the following likely short and medium term impacts on growth in new housing stock (and associated population) in different regions of Australia.