The QSR/Fast Food industry in Australia is worth almost $21B and is expecting modest growth of less than 1% over the next 5 years. There are a number of reasons why the forecast for growth is predicted to flatten this includes;

- Decline in foot traffic and dine in due to Covid 19

- Increased competition from supermarkets

- Increased competition from non traditional QSR restaurants

- Increased focus on healthier food options

However when there is volatility in the world, history has shown that consumers seek comfort food as a way of coping and as a result, during and post Covid 19, the industry overall has done very well maintaining revenue albeit at reduced profits. In addition, demand for food delivery services has increased in some cases by 30% but profitability has declined as delivery aggregators get a large slice of the profit.

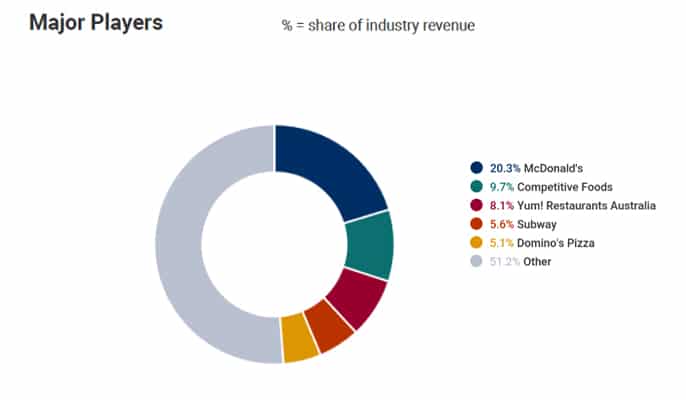

The pie chart below represents the breakdown by market share by revenue which clearly shows how dominant McDonald’s is in relation to the total revenue spent in this sector. With 1,000 restaurants in Australia, McDonald’s stands head and shoulders above the competition in market share of overall revenue.

Working closely with McDonald’s since 2016, Geotech has an intimate knowledge and understanding of what drives success for the brand…..they just do things differently on so many levels and constantly push us to refine and innovate always striving for that competitive edge.

This is part of the reason why Geotech is uniquely positioned to comment on the current state of the QSR market having partnered with a majority of the largest brands in Australia. In 1995, Geotech founder (Bruce Waddington) commenced his relationship with KFC (then owned by PepsiCo) a relationship that still exists today. KFC (now owned by Yum Brands) operates 650 restaurants in Australia with restaurant sales stronger than ever off the back of strong consumer demand for fried chicken.

The 10 biggest fast food franchises in the Australian market (by store numbers)

- Subway – 1300+ locations

- McDonald’s – 1,000+ locations

- Dominos – 694 locations

- KFC – 680+ locations

- Hungry Jacks – 420+ locations.

- Red Rooster – 360 locations

- Nando’s – 270 locations

- Pizza Hut – 254 locations

- Zambrero 181 locations

- Oporto 172 locations

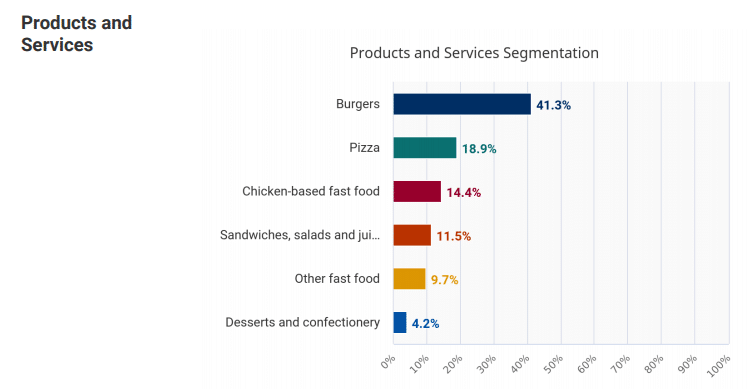

So what are consumers spending their money on? The chart below clearly shows that Australians love their burgers with over 40% of all fast food spending on this category.

Industry Outlook

Consumers have become increasingly concerned about fat and salt content. As a result, fast food operators have expanded their menus to include healthier options such as salads, yoghurt and wraps. New operators with a premium or healthy focus have also entered the industry to benefit from shifting consumer demand.

COVID-19 lockdowns and social distancing measures have seen an increase in orders through drive-through, instore pickup and food delivery services. However, with most operators relying heavily on passing foot traffic and lunchtime trade, moves towards working and studying from home have affected industry sales. The increased use of online food delivery services has also intensified competition from restaurants, as trading restrictions have led more restaurants to partner with food delivery platforms, such as Uber Eats and Menulog. This factor is expected to constrain industry demand in the current year, as consumers can opt for other cuisines and food establishments.

In addition, competitive pressures will likely force some smaller players to exit the industry, but this trend is forecast to be offset by an influx of new players in niche markets.

Growth in operator numbers will be driven by consumers shifting away from traditional fast food options towards healthier and higher quality alternatives.

Establishment numbers are also forecast to increase over the period, fuelled by well-established industry operators expanding their store networks.

New operators are anticipated to push employment numbers upwards over the next five years. However, competitive pressures in some segments will prompt operators to restructure and reduce operating costs, rein in wage expenses and close underperforming stores. In an attempt to improve profit margins, larger operators are forecast to undertake refranchising, selling licences for corporate-owned stores to new or existing franchisees.

Refranchising stores is a trade-off for franchisors, as it decreases marginal costs significantly but also relaxes the franchisor’s control over the store network. Without direct control, the franchisor risks declines in product and service quality. The franchisor may also have difficulty adjusting prices in response to shifts in trading conditions.