Delivery channel sales growth within the QSR and casual dining industry has been profound since Covid 19 shut down many locations to traditional ‘on premise’ activities in 2020.

Overall, the food establishments that had a well established multi-channel footprint did exceptionally well throughout the Covid storm, given most had already been serving customers through drive thru, takeaway & delivery.

Delivery in particular saw monumental growth, with increases in delivery in all types of suburbs, but particularly in suburbs that had been slower adopters of delivery prior, like the family and mortgage belt.

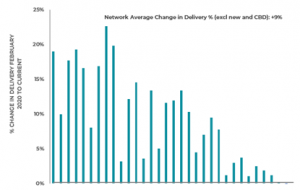

This move in who orders delivery, and from what type of outlets, resulted in variable delivery sales growth throughout Covid. The following is a typical example of what we saw in the market, with significant variability in restaurant delivery growth occurring.

You can see that some stores have achieved growth of 20% whilst others have grown by less than 5%. I bet many of you reading this would have a similar story to tell. Predicting delivery channel performance is extremely difficult, given the aggregators have not come to the party with any meaninful information to assist their clients which is another story in itself.

Sadly unlike other industries, more competition has not had a significant impact on aggregator fees, but what it did do was fast track app & loyalty data investment across the QSR industry, helping drive more traffic to app ordering and customer engagement. This is allowing operators to explore other options (like curbside pick up) and to maintain greater control on the customer interaction and delivery data.

Fast forward to today, and after monumental growth from 2020 to mid 2022, things are starting to settle down to a ‘new normal’ across the QSR industry. Delivery channel sales has likely peaked for many brands (with a steady reduction occuring as people return to more activity ‘out and about’), whilst others might still be growing steadily but not uniformed across the network.

There are three key things we’ve learned about delivery channel sales analysis in recent times that I would like to share;

- Delivery channel performance is not uniform, even in neighbouring suburbs, and with delivery a much greater slice of the sales pie, predicting delivery sales becomes more important than ever. Traditionally strong delivery channel performance was mainly confined to inner urban areas with a high proportion of young adults 20-35 years old. Due to Covid impacts this is no longer the case, with delivery channel performance extending out to outer suburban growth areas.

- There is a strong positive correlation between a stores positioning, signage, branding and appearance and delivery sales performance. The bricks and mortar store itself is a very important ‘call to action’ for ordering delivery. Up to 20% of delivery sales will be driven from a customer seeing the store and ordering that night. Therefore, increasing delivery is not an excuse to skimp on the quality of the bricks and mortar facility!

- Delivery channel cannibalisation impacts are more severe than we experience in the traditional dine in/take away sales channels. Once a customer has made the decision to buy a product online, the aggregator chooses the store that ends up taking the order and getting the sale. In contrast, not all visits to a restaurant are pre planned or destinational, and customers can maintain a preference / bias to an existing store, even if a new one opens closer. Consequently, the delivery channel will usually suffer higher cannibalisation than the traditional restaurant channel.

If you want to learn more about sales or cannibalisation forecasting methods or planning for delivery, please reach out to me for a confidential chat via email [email protected] or by calling me on 0421 684 444.